6 Group Health Insurance Integrated HRAs or Group Coverage HRA Designs for Just $199

$199 one-time fee in PDF via email*

$249 one-time fee in PDF email* + Deluxe Binder

With nearly unlimited design flexibility, employers can customize a Group Coverage HRA (GC-HRA) plan to seamlessly integrate with and enhance an existing group health insurance plan. A properly designed GC-HRA can reimburse a wide range of tax-free supplemental benefits, including dental, vision, deductible gaps, copays, coinsurance, Medicare-related expenses, retiree benefits, and more.

ABOUT CORE HRA PLAN DOCUMENT PACKAGE

05:00 Minute Executive Summary:

PDF Brochure: Core HRA Plan Document and Forms

Core HRA Plan Documents available in 2024

Section 105 HRA for one employee or spouse available since 1954, dubbed HRA in 2004 by the IRS and limited in 2014 by ACA. After the Affordable Care Act the HRA for 2 or more employees had to be integrated with employer sponsored group health insurance. The following six HRA design options are available.

-

-

- Comprehensive HRA Plan Document can pay any or all expenses not covered by the insurance plan (see IRS Publication 502 ).

- Deductible Gap HRA Plan Document allows employer to buy a cheaper $5,000 deductible. Employee only pays $2,000 deductible. Employer sets up HRA to pay $2,001 to $5,000 with premium savings.

- Limited HRA Plan Document for any specific charge or combination of charges such as dental, large hospital copay, etc.

- Medicare HRA Plan Document allows groups with less than 20 employees for employees who prefer Medicare as Primary Payer.

- Retiree HRA is set up specifically for retired employee benefit payouts.

- Excepted Benefit HRA (EBHRA) started Jan 1, 2020 integrated with employer group health and pays $2,100 a year (2024) for excepted benefits such as dental, vision, chiropractic, etc.

-

Qualified Small Employer HRA (QSEHRA) available Jan 1, 2017 for employers with less than 50 employees without group health insurance to pay individual health insurance and out-of-pocket medical. Annual limits apply, for 2024: $6,150 Individual and $12,450 Family.

Individual Coverage HRA (ICHRA) available January 1, 2020 for employers of any size without group health insurance to pay individual health insurance and out-of-pocket medical.

Section 105 HRA for one employee or spouse available since 1954. The Section 105 HRA is unique because the Affordable Care Act (ACA) did not consider a one employee HRA a group health plan. It escaped many of the limitations of the 2+ employee HRA plans after the ACA.

The HRA plan document is currently discounted to just $199 from $299 in a one-time fee. The Plan Document only needs to be updated when there are changes in the Code or ACA law, or if you want to change the Plan eligibility or benefit offering.

Under IRS and Department of Labor guidelines, employers simply need to adopt a formal HRA Plan Document and Summary Plan Description (SPD) that clearly outlines the benefit structure in writing. Once implemented, employers and employees may immediately begin enjoying valuable tax savings and enhanced benefit protection.

Everything an employer needs to know

Learn all about Health Reimbursement Arrangements by scrolling through the article, or go directly to one of these sections:

Small employers with no group health plan can provide a QSE-HRA to reimburse employees who obtain their own health insurance.

Introduction

The Health Reimbursement Arrangement (HRA) is a medical expense reimbursement plan funded by an employer for its employees. Reimbursements through an HRA are tax-deductible for the company and tax-exempt for employees.

HRAs have been popular with employers for decades. All of the costs were tax-deductible for employers and all of the rules and plan options were decided by employers.

And, there was no interference from the government until 2002, when the IRS issued formal guidance in Notice 2002-45.

The Notice defined the HRA, in part, as an employer-provided arrangement which:

-

- Is paid for solely by the employer

- Is excluded from the employee’s gross income (tax-exempt),

- Reimburses the employee and dependents for medical care expenses,

- May only provide benefits that reimburse expenses for medical care as defined in § 213(d),

- Requires substantiation of each medical care expense submitted for reimbursement,

- Provides reimbursements up to a maximum dollar amount for a coverage period,

- Allows that unused balances at the end of the year may be carried into the following year,

- Is subject to HIPAA privacy and COBRA continuation rules,

- Must be established with a written plan document and a copy of the plan document’s Summary Plan Description given to every eligible participant.

New ACA rules

When the Affordable Care Act arrived, HRAs took a hit. Popular plans that employers had long used to reimburse employees who bought their own health insurance were disallowed by the new law, and HRAs with a group health plan could only offer plans that carry all the new ACA-required essential health benefits with accompanying higher premiums.

A lot of employers lost their ability to provide an HRA to their employees on the same terms as before, while others could no longer afford the new group health plans the ACA required. It was a hardship for many employers and employees alike.

ACA relief for small employers

Eventually, small employers found relief from the ACA through the Qualified Small Employer HRA. Legislated through the 21st Century Cures Act of 2016, this ‘new’ HRA returns the ability for employers with fewer than 50 employees (and therefore not under the mandate) to once again provide a stand-alone HRA to reimburse employees buying their own health insurance.

More HRA options for 2024

In October 2017, President Donald J. Trump issued Executive Order No. 13813, Presidential Executive Order Promoting Healthcare Choice and Competition Across the United States. In part, it instructs the Departments of Treasury and Health and Human Services, “to increase the usability of HRAs, to expand employers’ ability to offer HRAs to their employees, and to allow HRAs to be used in

Less than two years later, in June, 2019, the President unveiled two new HRAs to do just that.

Available for plan years beginning on January 1, 2020, or later, the Individual Coverage HRA allows employers of any size to offer an HRA to reimburse individual health insurance premiums to employees and the Excepted Benefit HRA is designed to accompany a group health plan but may be elected by employees whether or not they participate an employer’s group health insurance.

HRA vs. FSA

The main difference between the HRA and Health FSA is that the HRA is funded solely by the employer while the FSA can be funded by both the employee and the employer.

Who funds the account determines how funds accrue and what happens with unused funds at the end of a plan year.

The FSA must be pre-funded. This means that when an employee elects to contribute $3,000 (through bi-weekly pre-tax salary deductions of $100 throughout the year), the employer must make the entire $3,050 available on day 1. This puts the employer at some risk of loss, though it is usually minimal.

With an HRA, the employer has the option to fund the account on a month-to-month basis. The employer also decides what happens with unused HRA balances at the end of the year and can allow employees to roll remaining funds over to the next plan year.

In contrast, an FSA, has a use-it-or-lose-it rule for balances that exceed the employer’s optional rollover allowance (up to $640) or 75-day grace period.

Limited HRA Plans can be restricted to just one type of expense, like prescription drugs.

Limited HRA Plans can be restricted to just one type of expense, like prescription drugs.

HRA Plan Flexibility

An HRA provides group health coverage to employees while employers enjoy optimum flexibility to save on group health premiums through customized plan design options.

Accrual options

As mentioned earlier, a Health Reimbursement Arrangement (Account) must be 100% employer-funded. This means maximum flexibility in how funds are made available and how fund balances can accrue.

First, the employer determines how much the HRA will provide for each employee in a plan year.

The next step is deciding whether that amount is available all at once on the first day of the plan year (pre-funded) or on a month-to-month basis.

Finally, carryover rules are set for unused fund balances at the end of the plan year.

Coverage types

Employers may choose the type of group health coverage that matches the purpose the employer intends for the HRA:

| HRA Plan Design | Reimburses for: | Coverage Type |

|---|---|---|

| Individual Coverage (ICHRA) | Individual Health Insurance premiums and related medical expenses. | Cannot offer group health insurance to employees offered an ICHRA. |

| Excepted Benefit (EBHRA) | Dental, vision, and other excepted health expenses. | Traditional Group Health Plan |

| Deductible-Gap | Expenses that fall within the “gap” in deductible with a group HDHP vs. traditional coverage | High-Deductible Health Plan (HDHP) |

| Comprehensive | Co-pays and co-insurance for medically necessary expenses. | Traditional Group Health Plan |

| Qualified Small Employer (QSEHRA) | Purchase of individual health coverage on the open market or exchange, and related medical expenses. |

No Group Health Plan (for employee groups of fewer than 50) |

| Section 105 HRA | Eligible medical expenses including health insurance premiums. | No Group Health Plan (1 employee) |

Year-end balances

Since employers fully fund all HRAs, the decision of carrying over or forfeiting all or a portion of unused HRA funds lies with the employer.

When an employer allows full carryover of the fund balance at the end of the plan year, employees may:

- Request reimbursement for medical expenses as they occur;

- Accumulate a balance for reimbursement in the future; or,

- Save the funds for retiree health benefits.

Popular HRA plan designs

Basically, there are two types of Health Reimbursements. Integrated HRAs require a group health plan while stand-alone HRAs not only do not require one, but usually forbid it.

Integrated HRAs

Deductible Gap

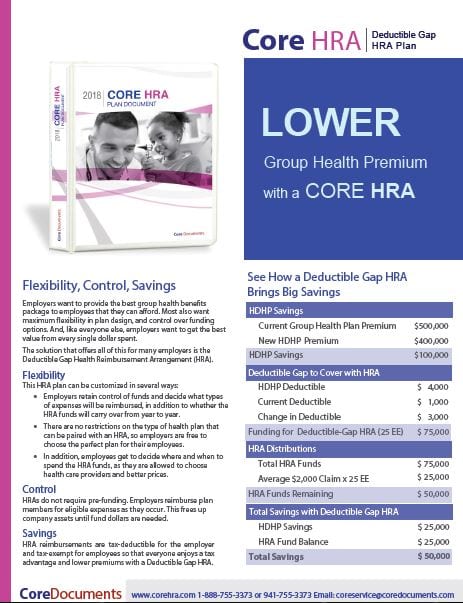

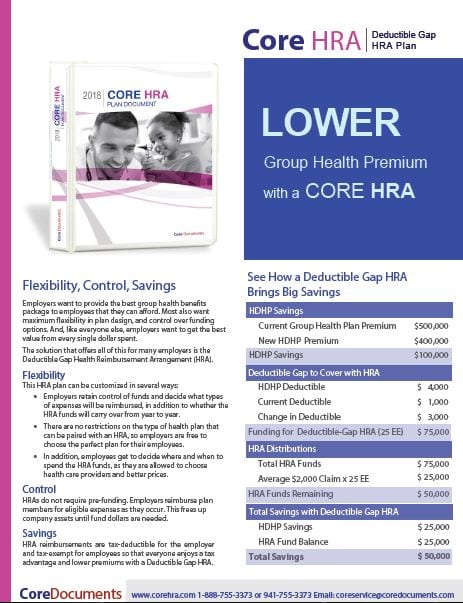

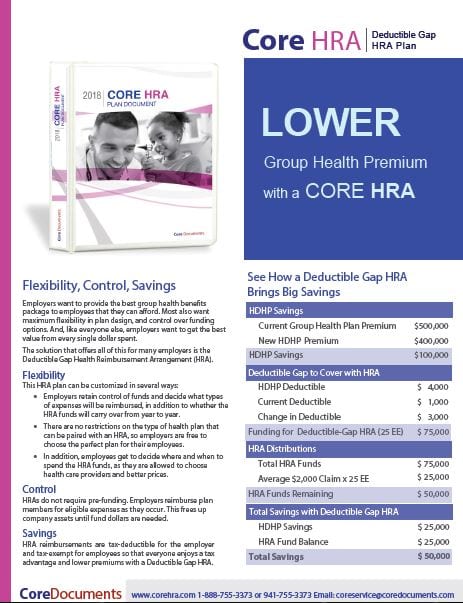

The Deductible Gap HRA Plan works with a larger high-deductible health insurance plan (HDHP). Example: The employer chooses a $5,000 deductible to reduce premium substantially. The employee only pays their regular $1,000 deductible and the Deductible Gap HRA pays the remaing $4,000 of deductible expenses. Once the deductible is met, the HRA no longer reimburses that employee for expenses for the year.

The employer saves by reducing its annual group health premium while the HRA cushions a large jump in deductible for employees. On average, about 20% of employees will have an expense that qualifies for deductible gap reimbursement.

This short video (1:09) shows how it works: How to Save on Group Health Premiums

Comprehensive HRA Plan

The Comprehensive HRA Plan is combined with a traditional employer-sponsored group health plan (including employees participating in a spouse’s or parent’s group health plan). It reimburses most 213(d) medically-necessary out-of-pocket expenses, including excepted benefit insurance premium expenses.

Video: Lower Group Health Premium with an HRA

Excepted Benefit (EBHRA)

The EBHRA is a new plan design that allows employers to reimburse employees for premiums and related medical expenses covering dental and vision care and other excepted benefits.

Stand-alone HRAs

Individual Coverage HRA

With an ICHRA, employers reimburse employees for individual health insurance premiums for individual coverage purchased on the open market or an exchange.

The employer decides the amount of expenses the HRA will reimburse for the plan year as well as whether it will reimburse premiums only or also reimburse other eligible medical expenses.

Employees must provide proof of eligible coverage. Medicare is eligible but no group health plan or STLDI (short-term) coverage can be integrated with an ICHRA.

Learn more: Individual Coverage HRA: Choice and affordability in employee health benefits

Video: The ICHRA video: Freedom from one-size-fits-all group health plans

Qualified Small Employer

A QSEHRA makes it simpler and more affordable for small employers to offer a more competitive employee benefits package.

For groups of fewer than 50 employees, a QSEHRA reimburses individual health coverage premiums that meet the minimum essential coverage (MEC) standard and qualified medical expenses.

Employers are limited to providing up to the annual limit of $5,150 for individual and $10,450 for family coverage (2019). Also, the employer must not have any group health plan for active employees.

Reimbursement rules require substantiation of expenses plus proof of MEC, which can be the employee’s purchased plan or evidence of coverage through a spouse’s or parent’s MEC plan.

This HRA coordinates with the ACA’s premium tax credit for individual or family health coverage purchased on the exchanges.

Learn more: Qualified Small Employer HRA Plan Document Package just $199

Video: A Better Group Health Insurance Alternative – QSEHRA

One-employee (or spouse)

Employers with one employee (for example, the spouse in a family business or the pastor for a church) can provide tax-saving health benefits for coverage that is not subject to the ACA’s essential health benefits or MEC rules.

A Section 105 HRA for one-employee groups reimburses the employee for health insurance premiums purchased on the open market or exchanges as well as eligible medical expenses not covered by insurance, including co-pays and deductibles.

Learn more: One-employee HRA Plan Document Package just $199

Employers save big on group health premium while an HRA bridges the gap for those employees that actually experience a higher deductible expense.

General rules for Health Reimbursement Arrangements

Employer contributions only

One reason HRA plans allow such flexibility in spite of tightening group health plan regulations is that it is funded entirely by the employer. No employee contributions are allowed in an HRA, which eliminates IRS concerns over a refund of pre-taxed employee contributions.

This also lets employers keep control of funds and to decide what expenses are reimbursed through the plan, a key point of flexibility popular in HRA plans.

Important: When integrated with a group health plan, employees may pay their portion of the premiums with pre-tax salary deductions; however, no portion of the HRA may receive employee dollars.

Group health plan options

Health Reimbursement Arrangements work with a variety of group health plan options, depending on the HRA plan design. The employer may choose traditional group health insurance for employees or a high-deductible health plan.

Employers choosing the ICHRA, QSEHRA, or Section 105 one-person HRA plan designs do not sponsor a group health plan at all, but reimburse the employee for individual health coverage premium instead.

Tax-exempt for employees

Reimbursements through an HRA are tax-deductible for the employer and tax-exempt for employees. This means that everyone enjoys a tax advantage when an employer chooses an HRA.

HRA Plan Document Required

The Code requires that the HRA plan be in writing and that every participant receives a Summary Plan Description, (SPD).

Prohibition on mid-year changes does not apply

The 12-month period of coverage and prohibition of mid-year changes do not apply to an HRA.

COBRA

HRAs are generally subject to COBRA continuation coverage requirements unless the small employer exemption applies.

Nondiscrimination Rules

HRAs cannot discriminate in favor of highly compensated employees or between individuals in the same class of employees.

However, employers can differentiate between amounts provided for individual coverage vs. family coverage and, in some cases, provide higher amounts for individuals age 50 and over.

Owner participation

Sole proprietors, partnerships, regular corporations, S corporations, limited liability companies (LLCs), professional corporations, and 501(c)3 non-profits are all allowed to establish an HRA Plan for the benefit of their employees.

Generally, however, the owners of said entities cannot participate in the HRA. This includes sole proprietors, partnerships, and LLCs; there are special exceptions owners of C corporations in integrated HRAs.

More resources

Ordering information

Enter your plan information safely and securely into our order form. If something is missing or we need to clarify an answer with you, we’ll contact you right away.

Usually, Core HRA plan document orders received by 3 P.M. eastern time, Monday through Friday, are completed and returned to you the same day.

![]()

Core Documents, Inc., accepts all major credit and debit cards, and e-checks. Just click on an order button to get started:

| Deductible Gap, Limited, Comprehensive, or PRA plan document | $199 |

Order Online |

| Excepted Benefit HRA plan document | $199 | Order Online |

| Individual Coverage HRA plan document | $199 |

Order Online |

| Qualified Small Employer HRA plan document | $199 | Order Online |

| One-Person Section 105 HRA plan document | $199 | Order Online |

Order your Core HRA package today!

Order your Core HRA package today!

Contact us

Want to make sure you’re choosing the best options to reduce group health premiums for your particular situation? Get in touch with a Health Reimbursement Arrangement plan design expert. Send us an email or call our friendly, knowledgeable staff at 1-888-755-3373

Brochures

|

Click image to open Core HRA brochure. |

Click image to open Core QSE brochure. |

Click image to open Core 105 brochure. |

HRA Comparison Chart

Get a quick overview of all HRA plan designs — including the new 2020 models — with this handy chart:

Click image to open the HRA Comparison chart.